FINANCE, BANKING & DEBT

LITIGATION ROADMAP

(List of Disputes Is indicative and not exhaustive)

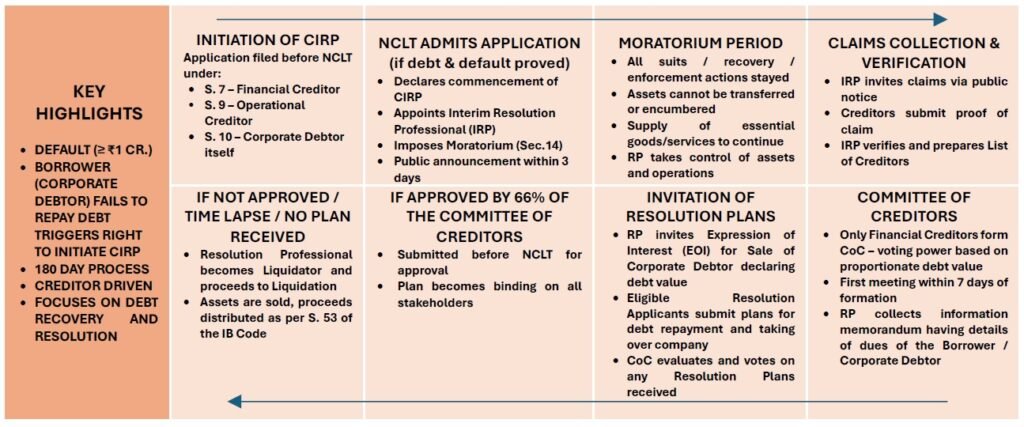

WHAT’S CIRP?

(Corporate Insolvency Resolution Process)

KEY LEGAL DEVELOPMENTS

- Bank has to remain vigilant and is responsible for detecting and preventing fraudulent transactions in bank account. Once duly reported, it is the Banks’ responsibility to refund and Account Holder has Zero Liability – Supreme Court

- Debt need not always be proved by a written contract – NCLAT

- No service tax payable for catering services provided to educational institutions – CESTAT

- Debtors statement to enter into an OTS with Creditor is proof of debt and default – NCLAT

- It is the bounden duty of the borrower to intimate the creditor of any change in address, cannot plead non-service if Demand Notice sent to previous address in case of non-intimation – NCLAT

- Director also liable for dishonour of cheque by company if he is in charge of and responsible to the company for the conduct of its business – Supreme Court

- Corporate Insolvency Resolution Process cannot be continued once debtor has repaid the entire debt – NCLAT

- Disputes between Banks over secured assets cannot be resolved by Debt Recovery Tribunal, have to be resolved by Arbitration – Supreme Court

- Advance consideration for supply is operational debt enabling Petition for Insolvency – NCLAT